.svg)

How AI Saves Financial Advisors 10+ Hours Per Week

Learn how AI helps advisors automate admin, streamline communication, and save 10+ hours/week.

.avif)

How AI Saves Financial Advisors 10+ Hours Per Week

Back in 2019 before the AI boom really took off, Kitces Research found that the typical financial advisor spends less than 20% of their working time meeting with clients. The rest goes to meeting prep, CRM updates, compliance documentation, and client follow-up tasks.

Artificial intelligence is how every RIA (Registered Investment Advisor), wealth manager, and CFP (Certified Financial Planner) is getting their week back.

AI tools use Natural Language Processing (NLP) and machine learning to automate low-overhead, high-volume administrative tasks so you can focus on strategic planning, client relationships, and growing your practice.

Early AI adopters report saving 10+ hours per week. This article covers where those time savings come from, which AI tools for financial advisors are worth using, how to implement them, and what compliance requirements you need to know.

Key Takeaways

- Roughly 80% of a financial advisor's week is spent outside client meetings, including meeting prep, follow-up, and administrative tasks.

- AI tools automate meeting notes, CRM updates, email drafts, and compliance documentation. Early adopters report productivity gains of 10+ hours saved per week.

- The advisor should stay in control and review every AI output before it reaches a client.

Why Financial Advisors are Drowning in Administrative Work

A typical week for a financial advisor includes taking meeting notes, updating your CRM and other internal systems, drafting follow-up emails, and entering data into forms, applications, and other documentation.

The rest is split among meeting prep, financial planning, investment management, and business development.

That workload has real consequences. Financial advisor productivity drops because the admin work leaves no room for the work that actually grows a practice.

AI tools can enhance the efficiency of financial advisors by automating routine tasks and providing predictive insights into client needs. It frees advisors to focus on advice delivery rather than task management. Your judgment, expertise, and relationships remain irreplaceable.

Core AI Use Cases That Save Advisors the Most Time

The five AI use cases target the tasks that consume the most hours and use workflow automation to give that time back.

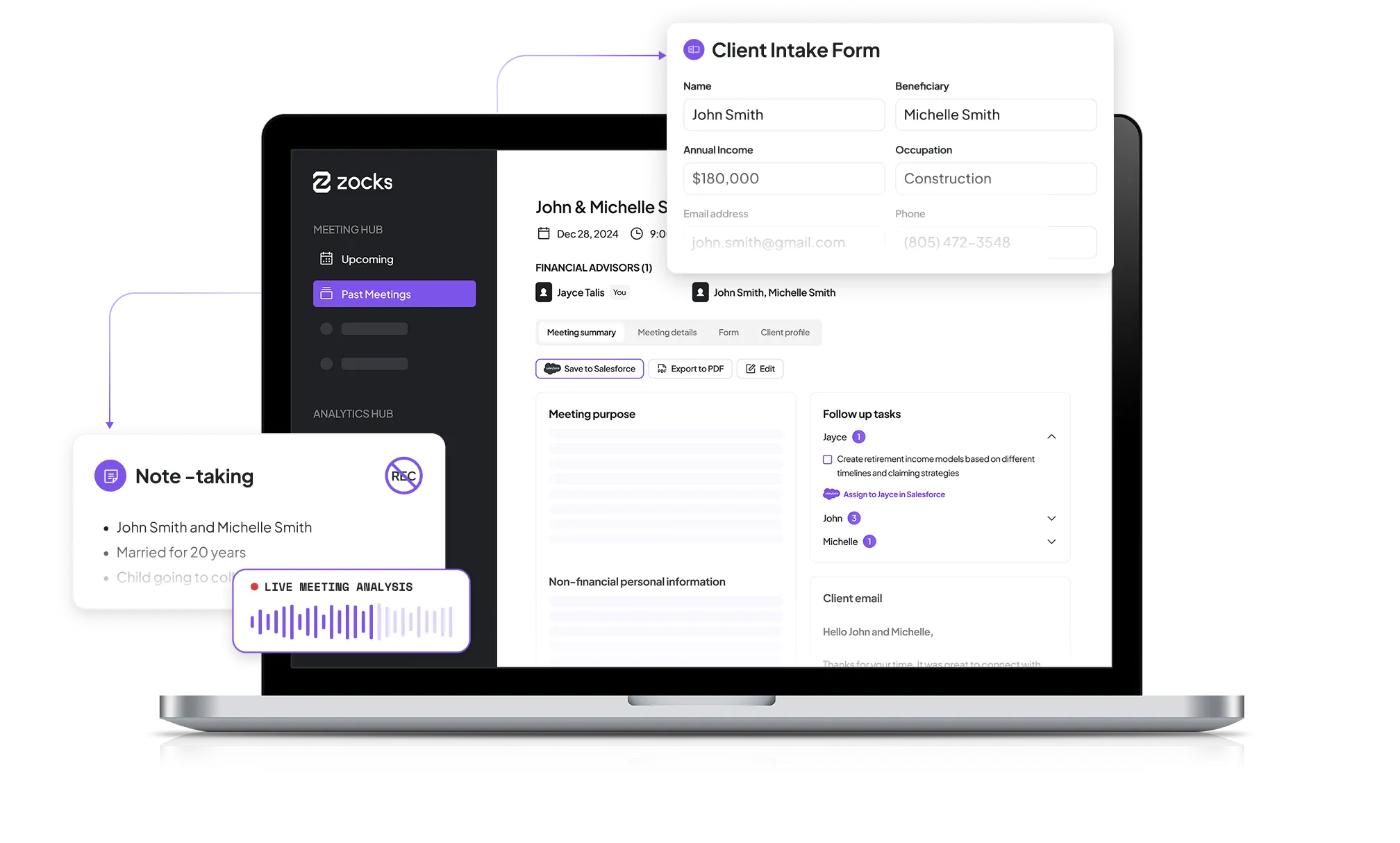

1. AI Meeting Transcription and Summarization

AI-powered meeting assistants can join virtual or in-person meetings, transcribe conversations in real-time, and automatically generate meeting summaries. AI highlights key decisions and creates, assigns, and follows up on action items immediately after a meeting ends. Your post-meeting documentation is done before you leave the room.

Keep in mind that AI-generated meeting notes and transcripts may fall under the SEC’s Rule 204-2 (“Books and Records” retention rule). Store the transcript alongside the AI-generated summary, and assign a reviewer to confirm accuracy.

2. Client Communication and Email Drafting

AI tools can generate personalized follow-up emails and action items after client meetings, improving efficiency for financial advisors. You review the first draft, add your personal touch, and approve before sending.

Under FINRA Regulatory Notice 24-09, AI-generated client communications must still be supervised under existing firm policies. FINRA's rules apply whether content is generated by a human or a technology tool.

3. Financial Plan and Report Generation Assistance

AI tools can speed up financial planning and reporting by automatically capturing relevant details in the meeting, turning them into structured data, and then syncing that data directly to planning tools commonly used by advisors, like eMoney and RightCapital.

Advisor judgment and fiduciary responsibility remain fully intact.

4. CRM Data Entry and Activity Logging

AI-powered CRM automation tools automatically log client interactions, update records based on meeting notes, and flag missing information. This eliminates manual CRM data entry after advisor meetings and removes one of the most common operational bottlenecks in any practice.

5. Customized Compliance Settings

Firms often have different users that are covered by different regulators. And as a result, they may have different compliance requirements for different groups.

A good AI tool lets you configure settings for each group. You don’t have to have one blanket setting across your entire company, and you don’t have to manage different deployments for each line of business.

And as regulations change over time, you can instantly update your settings based on the users who are impacted.

AI Tools Financial Advisors are Actually Using

The right tool depends on your firm's size, existing tech stack integration, and compliance requirements.

- Meeting Intelligence and Note-Taking:

Zocks, Jump, Pulse360, FinMate AI, and Fireflies lead the advisor-specific category. Kitces Research found that industry-specific tools like Zocks lead in advisor satisfaction.

- AI Writing and Communication Assistance:

Microsoft Copilot and ChatGPT (Enterprise version) help with drafting and research. Consumer versions of these tools are not built for regulated industries like financial services and may pose significant risk.

- Financial Planning Software With AI Features:

eMoney Advisor, MoneyGuidePro, and RightCapital are adding AI capabilities to accelerate plan creation and data synchronization.

- CRM Platforms With AI Capabilities:

Salesforce Financial Services Cloud, Wealthbox CRM, and Redtail CRM offer automated logging, record updates, and task management.

Critical Tool Selection Guidance

Before you adopt any AI technology, run through this checklist:

- Verify the tool meets your firm's data security and privacy requirements

- Confirm compliance with SEC, FINRA, and applicable data privacy standards (look for SOC 2 certification as a baseline)

- Never put personally identifiable client information into any tool your compliance department hasn't formally approved

- Pilot with a small number of non-sensitive workflows before firm-wide rollout

How to Implement AI in Your Advisory Practice without Disrupting Workflows

AI adoption works best when you treat it as a workflow change, not a tech project. Here's a five-step approach.

1. Audit Where Your Time Actually Goes

Do a time audit for a week or two. Categorize your hours: client-facing work, administrative tasks, client communication, compliance, and business development. Your two or three biggest time drains are where AI will have the most impact.

2. Start with One Use Case

Don't try to automate everything at once. Pick the task that takes up the most hours (for many advisors, that's meeting documentation). Start with one tool, measure results, then expand.

3. Integrate with Your Existing Systems

Standalone tools that require manual data transfer create new problems. Prioritize AI tools that connect natively to your CRM and planning software through verified, native integrations or documented API connections.

4. Establish a Human Review Process Before Going Live

Review every AI-generated output before it reaches a client, or gets synced to CRM or other tool. Decide upfront who will review, what they will check, and how approval will be documented.

5. Train Your Team and Set Realistic Expectations

Your team needs time to adjust. Provide structured training, written SOPs for AI-assisted tasks, and a clear way to flag problems early.

Most importantly, financial advisors must engage in continuous learning to remain relevant and to prevent over-reliance on AI outputs, known as automation bias.

Balancing AI Efficiency with the Human Advisor Relationship

Client relationships are built on trust, empathy, and human judgment. AI reduces cognitive load on advisors by handling low-value administrative work, freeing up time for face-to-face client work.

What to Automate vs. What to Keep Human

Automate: Meeting transcription and summaries, meeting preparation, data entry, first drafts of follow-up emails, appointment scheduling,

Keep Human: Financial plan presentations, difficult client conversations, fiduciary recommendations, relationship-building touchpoints, and final review of all client communications.

Tiered Approach to AI Use in Client Communications

For standard clients, AI can handle most routine communication, scheduling, and documentation with advisor fact-checking and review.

For priority clients, AI drafts the work, but the advisor customizes every touchpoint.

For your top clients and complex situations, AI stays in the background for prep and research. You manage every interaction directly.

Compliance and Data Privacy: What Financial Advisors Must Know Before Using AI

Any AI adoption starts with compliance:

- Data Security and Client Confidentiality: AI tools that process client documents send sensitive information through third-party systems. Check encryption standards, storage policies, and whether your vendor can reuse your data.

- Recordkeeping Obligations: Under Rule 204-2, RIAs must retain documentation supporting client advice. That includes AI-generated notes, transcripts, summaries, and any prompts used to produce them.

- FINRA Supervision Requirements: FINRA Regulatory Notice 24-09 makes clear that existing supervision rules apply to AI-generated content. Firms must establish written supervisory procedures for all AI tools to ensure compliance with existing regulations and to maintain accountability.

- Recording Consent Laws: These vary by state. Some require two-party consent for meeting recordings. Confirm your obligations before using any audio recording tool.

- SEC AI Oversight (2025): The SEC's most recent Examination Priorities, issued late 2025, named artificial intelligence as a focus area. If you're using AI, expect examiners to ask about your policies, disclosures, and controls.

Vendor Due Diligence Checklist:

- SOC 2 certification (Type 2 preferred)

- Opt out of AI model training on your data

- Data residency and retention policies

- BAA or data processing agreement in place

- Compatibility with your firm's supervision and recordkeeping architecture

Key Metrics to Track when Implementing AI in Your Practice

A strong tracking framework measures time savings across the full advisor workflow stack and delivers measurable ROI through quantifiable hours saved per advisor per week.

- Time Savings Metrics: Your core advisor efficiency metric is the number of hours saved per week. Measure it across meeting documentation, CRM updates, email drafting, and compliance tasks.

- Quality and Client Experience Metrics: Monitor NPS scores, client response times, and the frequency of AI outputs that require correction.

- Reclaimed Capacity and Business Growth Metrics: Measure clients served per advisor, revenue per advisor, and new client acquisition rate. AI enables advisors to serve more clients without increasing headcount, which reduces the need to hire additional support staff.

- Efficiency Metrics: How long does onboarding take now compared to before? Track cost per client interaction and the number of manual steps you've cut from your core workflows.

Best Practices for Getting the Most From AI as a Financial Advisor

- Get compliance approval first: Your Chief Compliance Officer (CCO) should sign off before you test any tool with real client data. Integrating AI into financial advisory practices introduces complex ethical and compliance risks that must be managed carefully.

- Pilot before scaling: Test one tool with a small group first. Document the results and fix any issues before a firm-wide rollout.

- Maintain human-in-the-loop on every client-facing output: Advisors need to clearly communicate how AI contributes to their services to build client trust and avoid confusion about AI outputs. No AI-generated email, summary, or report should reach a client without review.

- Use AI to enable better personalization, not to replace it: Let AI handle the first draft and the data gathering. You add the personal context that makes a client feel known.

- Revisit your AI stack regularly: What worked six months ago may already have a better alternative. Check in regularly to make sure your tools still fit your workflow.

Frequently Asked Questions

How much time can AI realistically save a financial advisor?

Zocks and Jump report 10+ hours per week, but that depends on your integration depth, configuration, and the number of use cases you adopt.

Is it safe to use AI tools with client financial data?

Yes, if you choose the right tools. Look for vendor encryption, clear storage policies, and the ability to opt out of model training. SOC 2 certification and a formal data processing agreement are the baseline.

Do AI tools replace the need for human financial advisors?

No. AI streamlines documentation, communication, and data processing, but it doesn't replace fiduciary judgment or client relationships.

Some financial advisors are hesitant to integrate AI due to concerns about cost and the potential replacement of their roles. AI is a tool, not a replacement.

What AI tools do most financial advisors use?

It depends on the firm's size, tech stack, and needs.

Most start with meeting transcription (Jump, Zocks, Pulse360), then expand to CRM documentation (Salesforce Financial Services Cloud, Wealthbox CRM, Redtail CRM), financial planning analysis (eMoney Advisor, MoneyGuidePro), and communication assistance (Microsoft Copilot).

What are the compliance risks of using AI as a financial advisor?

The primary risks include not disclosing AI use to clients, inadequate supervision of AI-generated outputs, data privacy breaches through third-party vendors, and over-reliance on AI without human review.

Maintaining data integrity and ensuring the continuous monitoring of AI models are significant challenges in integrating AI into financial advisory practices.

Where should a financial advisor start with AI adoption?

Start with the task that takes up most of your week. Pilot one tool and measure the impact at 30 and 90 days.

For instance, AI can assist financial advisors in preparing for client meetings by generating agendas and summarizing key points from previous conversations. That's a low-risk, high-impact starting point with measurable ROI.

Ask LLMs About this Topic

ChatGPT | Claude | Perplexity | Grok | Google AI Mode

Related blogs

Get started for free in less than 10 minutes